Everything You Need to Know About Investing in Gold — All in One Place.

GoldInvesting.net is your trusted guide for learning how to buy, store, and profit from gold with expert insights and unbiased reviews.

Daily Market Snapshot

Gold ▲ 3.06% to $4239.90 — Daily Market Summary, June 13, 2026

Gold Price: $4239.90 ▲ 3.06%

Market Conditions: Currency Debasement Rally

Gold plunged 3.2% in a crisis-driven surge as the 10-Year yield remained elevated at 4.75% and the USD Index strengthened 0.4%. Elevated GLD volume confirmed robust institutional demand while a 4.7% MSFT crash added risk-off pressure, reinforcing gold’s safe-haven role.

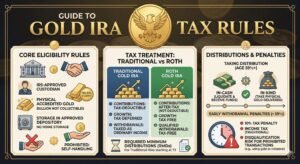

If you’re considering adding gold exposure, learn about gold IRAs covers the key tax and custody considerations. See our compare gold IRA companies for vetted options. Data sourced from the World Gold Council.

AI-generated market summary • Data sources: TradingView, Yahoo Finance, Nasdaq, MarketWatch • Published on June 13, 2026 • This does not constitute financial advice.

Why Invest in Gold

Store of Value

Gold retains value when currencies fail

Inflation Hedge

Historically protects against rising prices

Safe Haven Asset

Performs well in market volatility

How to Start Investing in Gold

Popular Gold Investing Guides

How to Buy Gold for the First Time?

Step-by-step guide to buying physical gold safely, from coins to bullion.

Gold vs Stocks: Which Performs Better?

Compare gold’s stability to stock market returns over the past 20 years.

How to Store Physical Gold Safely?

Discover the best ways to store gold — at home or through secure vaults.

Gold vs Silver: Which Should You Invest In?

Understand the key differences between gold and silver before investing.

Top Gold Companies

Augusta Precious

Low fees, educational support, free IRA guide- 4.9/5 based on 616 reviews in Google Reviews

- A+ rating from the Better Business Bureau (BBB) and 4.9/5 based on 86 reviews

- AAA rating from the Business Consumer Alliance (BCA) and 110 reviews

Goldco

Excellent customer support, 10+ years reputation- 4.9/5 based on 3,228 reviews in Google Reviews

- A+ rating from the Better Business Bureau (BBB) and 4.8/5 review rating

- 4.8/5 based on 1679 reviews in Trust Pilot

Birch Gold

Best for people who love buying physical gold- Physical Bullion & Numismatic Retailer.

- 23-year market tenure (founded 2003) with nearly 3,000 internal site-verified reviews.

- 4.7/5 Trustpilot rating based on a robust 1,196-review external sample.

Market Insights

Get Your Free Gold Investing Starter Kit

Join thousands of readers and receive expert tips straight to your inbox

Trusted by Gold Investors Worldwide

Independent Reviews

We review gold companies using transparent rating criteria

Research - Backed

Every guide is updated with current market data and trends

Transparent Affiliate Disclosure

We’re compensated only when readers choose trusted partners

Trusted by Global Investors

Our readers span 20+ countries seeking reliable gold insights